Following the last three years, a pause in risk assets was predictable—if not expected. We noted as much in our Q3 2025 Market Outlook, which was based not on the quality of our crystal ball, but on our belief that markets rarely deliver sustained, above-trend returns without some measure of consolidation. Markets were priced to perfection and the magnitude of the gains since 2023 only serves to make a correction all the more likely.

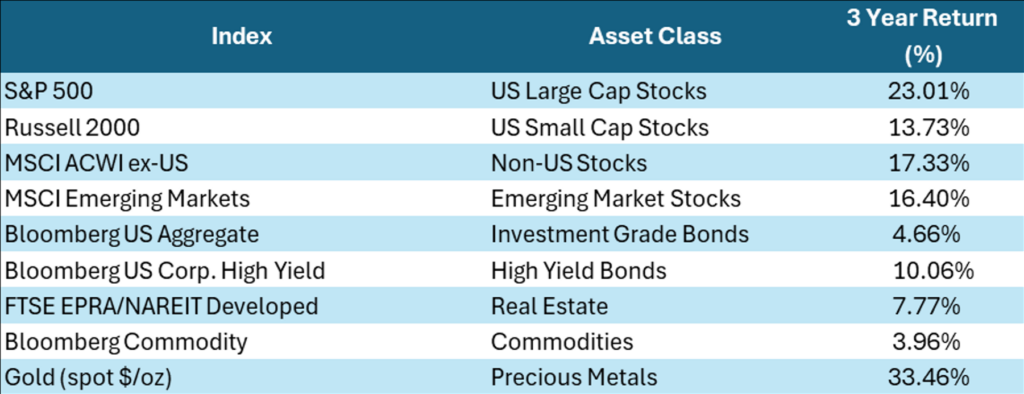

As a quick reminder of where we were, below is a chart with the annualized 3-year returns of major asset class indices, as of the end of 2025.

Returns were strong across most major risk asset classes, with high yield bonds compounding at just over 10%, small cap US equities closer to mid-teens, developed and emerging international equities producing solid mid- to high-teens returns, and US large cap equities standing apart at roughly 23% annualized. In most circumstances, a pullback would not have been surprising. What has unfolded so far this year, however, has not been as straightforward as a cyclical reset. Instead, markets have been digesting a series of overlapping developments that together have created a more fragile backdrop.

Why This Hasn’t Looked Like a Typical Market Reset

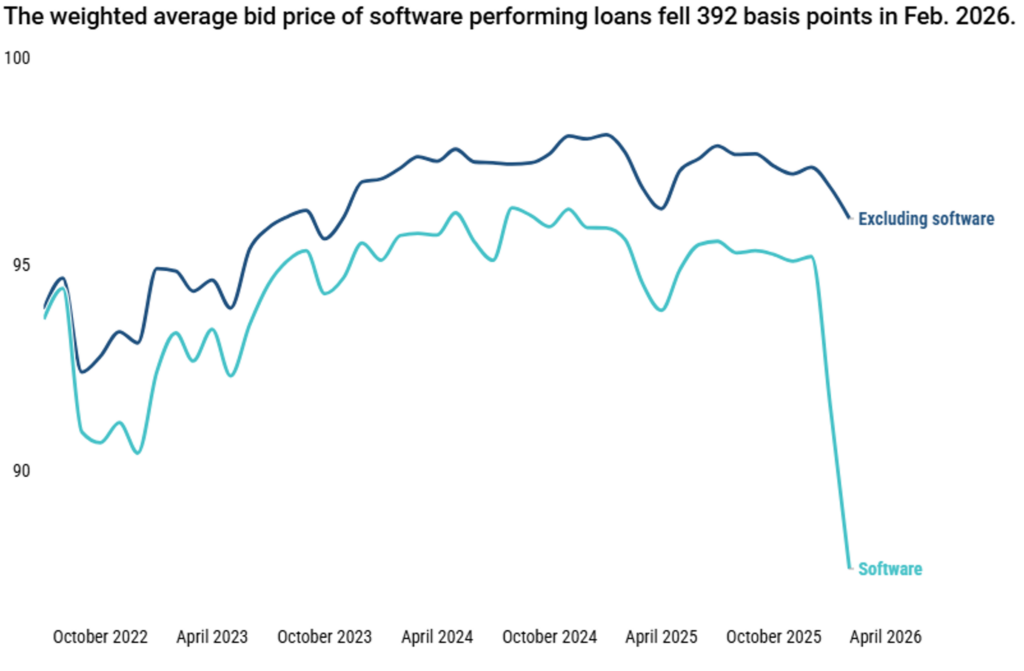

Given the lofty expectations (and investments) being placed on AI, it was logical to expect a pause—skepticism enters the equation and prices get rationalized. In many cases, skepticism yields to pessimism and prices overshoot on the downside. One could argue that the price action in software companies, which began weakening late last year, reflects this typical market cycle. This extended into the private credit markets, in another example of healthy market dynamics separating the wheat from the chaff. As the chart below indicates, private credit investors are increasingly seeing software businesses as requiring an additional risk premium when compared to all other sectors.

As we discussed in a recent update on the private credit markets, headlines that generalize private credit as a concern fail to reflect the nuance between different portfolio compositions and approaches to risk and return management. Ultimately, we would view the repricing of risk within technology, in both equity and fixed income markets, as being signs of a healthy pricing mechanism and, in many cases, overdue.

Managing through a normal cyclical correction is not particularly pleasant, but it is also not a cause for concern, as we’ve been through many ups and downs throughout our investing careers. The current added layer of policy and geopolitical turmoil, however, requires a closer analysis due to the compounding potential of negative events. That domino effect can turn a correction into a bear market, or a gradual economic deceleration into a recession. This is where the added diligence becomes critical.

No doubt, the elephant in the room is the current escalation of tensions between the US, Israel and Iran. However, before the bombing campaigns began, we were already dealing with uncertainty due to the ever-evolving nature of the global trade regulation and the persistence of stubborn inflation. The Supreme Court’s ruling on tariffs removed one potential source of cost pressure, but it did not restore clarity. Instead, companies are now having to navigate uncertainty around what comes next, including the mechanics and timing of refunds, the risk of litigation, and the likelihood that a different statutory path replaces the prior one. When the first round of tariffs was announced a year ago, we urged patience as we believed the actual realities would need to be negotiated and litigated over time. Almost a year later, while some trade agreements have been established, the lack of clarity remains a burden on our economy. On the inflation front, progress has been made, but it has been slow and now faces the added challenge of a potential energy shock.

Energy and Geopolitics Return to the Foreground

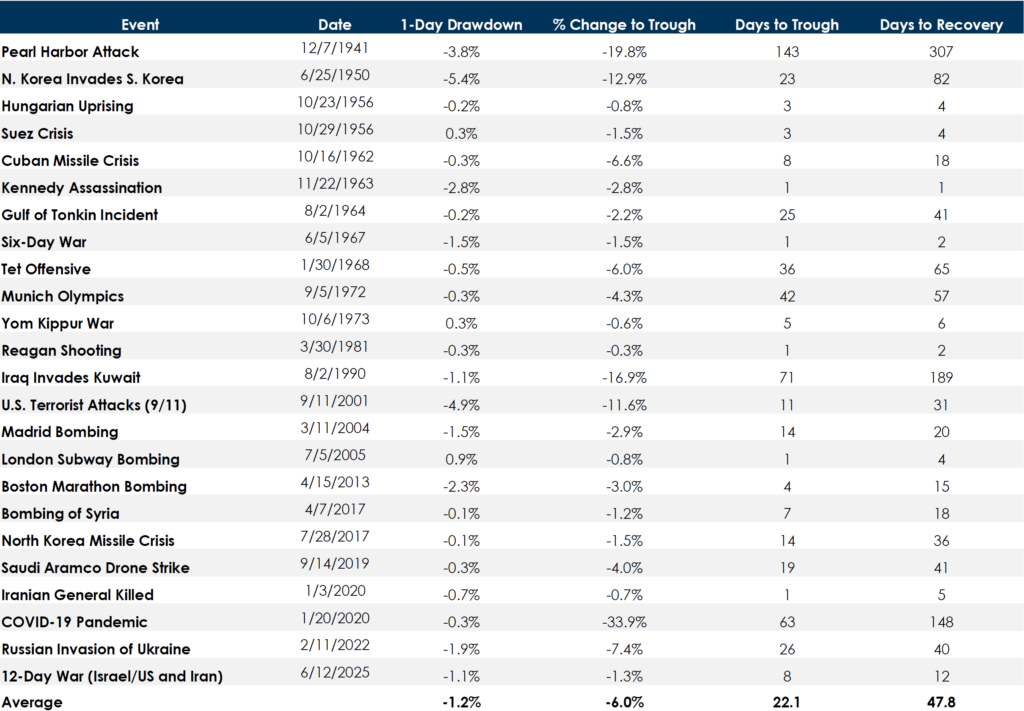

This brings us to a major domino that has fallen: the outbreak of war between the US, Israel, and Iran and the collateral damage across the region caused by extensive bombing and drone attacks. The table below from our colleagues at Asset Consulting Group summarizes the recent history of geopolitical shocks. This tracks with a note we sent out a few weeks ago, which bore the conclusion that, often, markets recover quickly from geopolitical shocks.

In isolation, we would easily conclude that the probability of a prolonged bear market would be low based solely on the outbreak of a regional war. A level of concern arises when we combine all the different layers of the current picture: AI-skepticism, trade uncertainty, geopolitical instability, stubborn inflation, and an energy shock.

A source of optimism heading into this year was the potential for monetary easing coming from the FOMC. According to the CME FedWatch tool, at the end of October 2025, futures markets were pricing in a ~70% chance of 2 or more rate cuts this year. Those odds have shifted materially due to sticky inflation readings in February and the potential for energy supply shocks resulting from a prolonged conflict in the Middle East. One key point of debate has been the duration of the conflict. Temporary disruptions can be managed and arbitraged, whereas multi-year outages must be repriced.

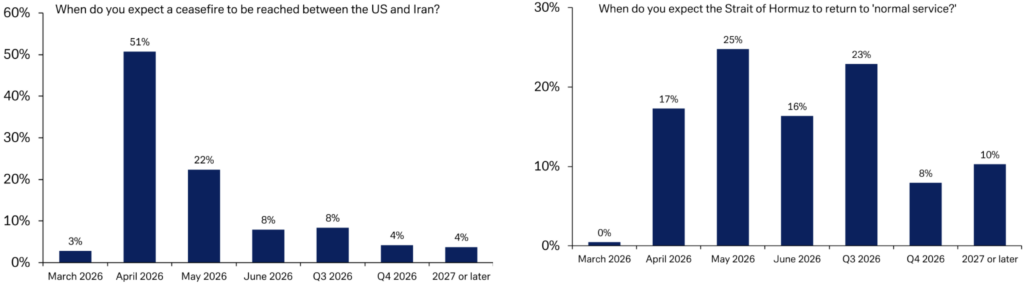

Interestingly, as the charts below from a recent Deutsche Bank survey highlight, approximately 74% of respondents believe a ceasefire will be reached by end of April. Additionally, over 80% of survey respondents also expect the Strait of Hormuz—a critical link in the global energy supply chain due to the volume of oil and LNG that traverse its waters—to resume normal operations by the end of Q3.

Accordingly, we have seen major producers start to use different means to circumvent the Strait of Hormuz. This recent article by Bloomberg News, highlights the flexibility that some countries have at their disposal.

This flexibility is not afforded to all nations, nor is it afforded to all forms of energy—Liquified Natural Gas (“LNG”) being a prime example. The missile strikes on Qatar’s Ras Laffan LNG complex are particularly worth noting. By QatarEnergy’s CEO’s own admission, this attack took approximately 17% of their LNG production offline, and the rebuilding process is said to be measured in years as opposed to months. According to the Institute for Energy Economics and Financial Analysis, the global production of LNG reached 474 metric tons per annum (MTPA) in 2024. With estimates pointing to approximately 12.8 MTPA being lost with the capacity of the two Qatari liquefaction trains, that amounts to 3% of global LNG supply being impaired and difficult to replace in the short-term. In the longer run supply and demand should stabilize, as planned projects come to fruition. The International Energy Agency expects capacity to expand by approximately 250 MTPA by 2030. In the meantime, net importers will have to contend with more uncertainty than they would have anticipated just 3 months ago.

Our ultimate read on the macro situation and its investment policy implications is summarized below:

Near-term, the environment is inflationary.

Energy remains a foundational input, and supply disruptions (real or threatened) tend to flow quickly into expectations. This matters because core inflation remains stubbornly above the Fed’s target, leaving limited room for clean and accommodative policy responses.

It does not change long-term discipline.

Time in the market has historically mattered far more than timing the market, especially around geopolitical events. As the chart below highlights, the greater risk lies in turning temporary uncertainty into permanent decisions.

Policy volatility is becoming structural.

The tariff ruling did not end uncertainty; it reshuffled it. Policy variability increasingly looks like a feature of the landscape rather than an exception. The trend of nationalism and deglobalization seems primed to continue unchallenged.

Keep an eye on sovereign wealth funds.

We believe in the strategic importance of building a programmatic private investment portfolio. Sovereign wealth funds are major participants in those markets. According to US News, four of the ten largest sovereign wealth funds are in the Middle East (UAE, Kuwait, Saudi Arabia and Qatar). If the conflict between the US, Israel, and Iran lasts longer than anticipated, further damages key infrastructure, or constrains a key source of revenue for the region. We will be monitoring the private transaction markets for any shift in investor appetite.

The Case for Diversification

Our industry has done investors a disservice by trying to argue a binary conclusion to the concept of diversification. Diversification is neither a panacea nor a waste of time. It is simply a recognition that concentrated bets, even when they are fundamentally sound, come with path‑dependency risk.

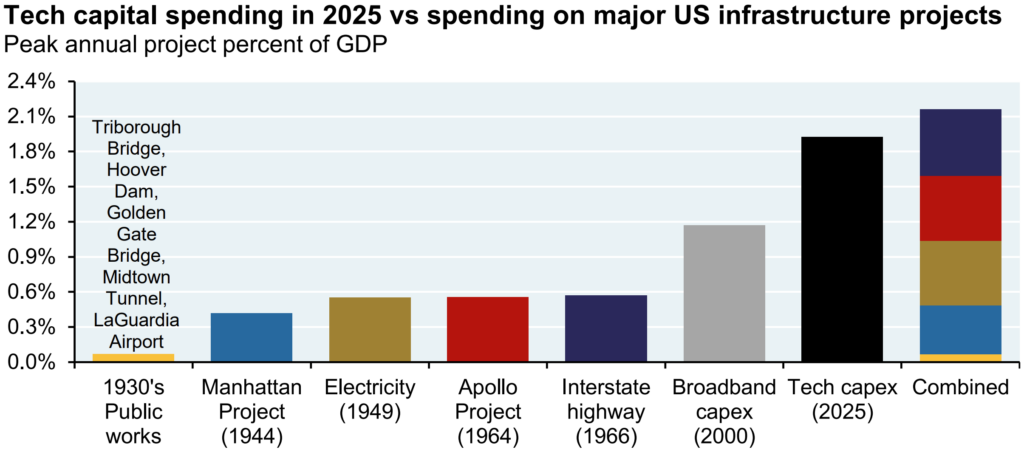

Today, that concentration shows up most clearly in AI. As the chart below from Michael Cembalest illustrates, hyperscaler capital expenditures are approaching levels previously reserved for national infrastructure projects.

Alphabet, Microsoft, Amazon, and Meta are expected to collectively spend on the order of $650–700 billion on AI‑related infrastructure in 2026 alone, according to reporting from CNBC. That scale of investment may ultimately prove justified, but it also narrows the margin for error and increases sensitivity to any disappointment in monetization timelines.

This concentration also shows up geographically. US equities have delivered exceptional returns, but those returns are increasingly driven by a small cluster of mega‑cap technology and tech‑adjacent firms. Information technology now represents roughly one‑third of the S&P 500, with a handful of names accounting for a disproportionate share of index performance. This does not invalidate U.S. exposure. It does, however, raise reasonable questions about home‑country bias, valuation dispersion, and whether the United States’ competitive moat is as static as we would all want to contend. While we are still firm believers in the dynamism of the US corporate ecosystem (and are meaningfully invested in its outlook and prowess) we believe that, at best, our competitive moat is stable. More likely, however, it is narrowing under the combined pressure of fiscal dynamics, political polarization, and the rapid diffusion of technological capability. While this falls squarely in the “talk” category, it is worth noting the recent discussions occurring in Europe surrounding the region’s desire to reduce its reliance on US-based cloud computing capacity. Any shifts are unlikely (or incapable) to happen overnight, but more attractive valuations outside the US, particularly in markets less dominated by a single growth narrative, deserve consideration.

Portfolio Implications

With that macro-perspective as our backdrop, the key question we must ask ourselves is what (if any) investment or policy shifts should we be implementing in portfolios. To that end, we think it is helpful to break it up into categories:

Maintain 12 months of lifestyle-required liquidity in cash, money market funds, or short-duration investment grade fixed income.

Given the constraints on the FOMC to ease monetary policy, and currently tight credit spreads, we see little reason to take duration or credit risk with capital that has known uses in the next 12 months.

Be ready to rebalance.

As markets swing between pessimism and optimism, dislocations frequently arise, and we are always looking to take advantage of the market overreacting in the short term. Since peaking in October last year, the Nasdaq is down almost 12% through March 25th a decline that meets the technical definition of a correction. Given the frequency of corrections (they occur on average once a year) we do not typically view these as rebalancing opportunities. That being said, we will be ready if we are presented with attractive entry levels.

Look for attractive return profiles with unique risk factors.

AI potential and its related investment spending have been, and are likely to be, the most influential growth factor driving markets in the near future. We’ve said it in the past, but it is worth reiterating: we are long-term optimists on the productivity and quality of life benefits AI represents. We believe it is prudent, however, to diversify our risk exposures and look for uncorrelated return opportunities.

An example of this concept is the work that we have been doing on healthcare credit—specifically strategies that provide financing to small- and mid-cap pharmaceutical companies at the commercialization stage. The success (or failure) of each company tends to be idiosyncratic and less sensitive to the market cycle—healthcare demand is widely considered to be inelastic—and we like the potential diversification benefits of outcomes that are untethered to the concentrated factors driving near-term market momentum. These are the proverbial singles and doubles of the investment world that we believe round out a prudent long-term investment strategy.

Final Thoughts

The world is a risky place, and there is no shortage of reasons to be concerned. But investors are rarely rewarded for treating every risk as existential. With hindsight, most prove not to be. The more productive approach is to focus on what remains within our control: liquidity planning, rigorous manager diligence (these are the environments where human error is most costly), disciplined rebalancing, and adherence to long‑term objectives. Underperformance does not necessarily imply failure; often, it creates opportunity. And if the objectives that led you to build your plan have not changed, the plan itself likely does not need to either.

About Thierry J.D. Brunel

Thierry joined Matter in 2013, bringing years of experience in family office and wealth management. He previously worked in investment research and portfolio management roles at Convergent Wealth Advisors and GenSpring Family Office. At Matter, Thierry leads the investment committee, advising families on portfolio strategy and governance. A Wake Forest University graduate, Thierry has a diverse international background. He’s active in his community, serving as an assistant coach for the John Burroughs School Varsity football team in St. Louis.

Other Investment Blogs

Important Information

This material is for information purposes only. The views, opinions, estimates and strategies expressed herein are based on current market conditions and are subject to change without notice. Any companies referenced are for illustrative purposes only, and are not intended as a recommendation or endorsement. Any views, strategies or products discussed in this material may not be appropriate for all individuals and are subject to risks. Investors may get back less than they invested, and past performance is not indicative of future results. Asset allocation/diversification does not guarantee a profit or protect against loss.

Nothing in this material should be relied upon in isolation for the purpose of making an investment decision. Certain information contained in this material is believed to be reliable; however, Matter LLC does not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. No representation or warranty should be made with regard to any computations, graphs, tables, diagrams or commentary in this material, which are provided for illustration/reference purposes only. Any projected results and risks are based solely on hypothetical examples cited, and actual results and risks will vary depending on specific circumstances.

Forward-looking statements should not be considered as guarantees or predictions of future events. Nothing in this document shall be construed as giving rise to any duty of care owed to, or advisory relationship with, you or any third party. Nothing in this document shall be regarded as an offer, solicitation, recommendation or advice given by Matter LLC and/or its officers or employees.